Blog

How Can US Insurance Leaders Build Explainable AI Models That Pass Compliance Review?

US insurance leaders no longer ask whether AI can improve underwriting and claims. They ask whether AI can survive compliance review when a customer, regulator, or internal audit team challenges a decision.

That shift changes the role of engineering. A model that improves speed but cannot explain a Premium change, a claim denial, a fraud flag, or a risk score poses a business risk. The problem does not start with data science. It starts when product, compliance, actuarial, and engineering teams build AI as separate workstreams.

KPMG’s 2025 Insurance CEO Outlook reports that 73 percent of insurance CEOs prioritize AI investments for underwriting, claims, and customer experience. This shows intent, but intent does not equal readiness. Many carriers still run legacy data pipelines, fragmented policy systems, and unclear model ownership.

A serious insurance app development strategy must treat explainability as part of the product infrastructure. The model should not explain itself after launch. The platform should capture why the model made a recommendation at the moment the decision happened.

Compliance Review Starts Before Model Training

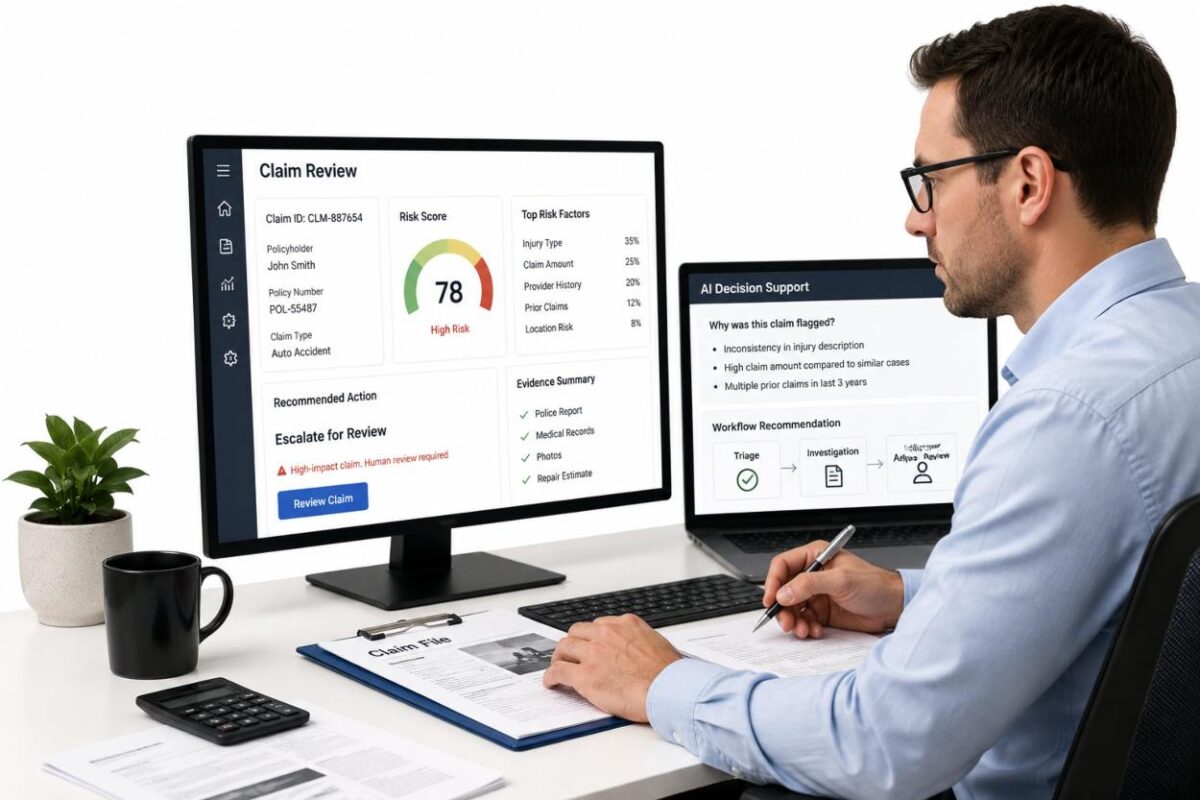

Insurance AI fails compliance review when teams treat explainability as a dashboard. A dashboard can show feature importance. It cannot prove that a carrier used allowed data, tested for unfair discrimination, and kept human oversight inside the workflow.

The NAIC model bulletin pushes insurers toward fairness, accountability, compliance, transparency, and secure AI systems. Colorado’s insurance AI rules have made this pressure real by targeting external data, algorithms, and predictive models that can create unfair discrimination.

The stronger position for 2026 is direct: insurers should not deploy black-box models in underwriting or claims unless the business can defend every decision in class.

That means engineering teams need three records inside the platform. They need a data lineage record, a model version record, and a decision explanation record. These records should connect to customer action, not sit inside audit folders.

One industry lesson deserves a simple quote: “Explainability without evidence is opinion.” Regulators do not need a story about responsible AI. They need proof that the insurer controlled the model, monitored outcomes, and corrected risk.

What Makes An Insurance AI Model Explainable?

An explainable insurance model provides business teams with a reason code humans can understand and an evidence trail that technical teams can test. These two needs differ. A customer service leader needs a clear explanation. A compliance officer needs traceability. A data scientist needs reproducible logic.

Underwriting models need local and global explainability. Local explainability answers why a specific applicant received a risk score or pricing band. Global explainability shows which features influence model behavior across states, products, channels, and customer segments.

Claims models need workflow explainability. A claim triage score should connect to documents, adjuster notes, damage images, prior claim history, fraud signals, model version, and final human action. Without that link, the carrier cannot separate model recommendation from operational judgment.

This is why machine learning development in insurance must include model observability, feature governance, role-based access, and audit logs from day one. The model matters, but the control system around the model matters more.

Underwriting Risk Leaders Cannot Ignore

Underwriting teams want sharper risk selection, faster quotes, and stronger loss ratios. AI can support those goals, but it can also expose the carrier to proxy discrimination.

Zip code, occupation, device data, social signals, payment behavior, and browsing patterns can correlate with protected traits. Even when a carrier removes prohibited fields, the model can learn proxies through related variables.

This makes feature governance a broad issue. Engineering teams should classify every feature as approved, restricted, sensitive, derived, or prohibited. They should record who approved the feature, why the business needs it, and which fairness tests apply.

The guiding principle for insurance leaders is simple: if a feature cannot withstand regulatory scrutiny, it should not enter the model.

Actuarial teams can still use risk signals. They need a controlled framework that proves business relevance and tests customer impact. The goal is not to weaken underwriting. The goal is to make underwriting defensible.

Claims AI Needs Human Judgment By Design

Claims leaders often use AI to reduce cycle time, flag fraud, prioritize files, and route complex cases. These gains matter, but claims AI touches customers during high-stress moments. A poor explanation can damage trust faster than a slow process.

A claims model should not act as an invisible authority. It should act as a decision support layer. Human adjusters need to see why the model flagged a file, which evidence shaped the score, and what action the workflow recommends.

Leaders should set clear rules for automation. Low-risk routing can use automation. High-impact decisions need human review. Fraud escalation, claim denial, settlement reduction, and special investigation triggers need stronger oversight.

One practical quote fits this operating model: “The human should not rubber stamp the model. The human should challenge it with context.” That mindset helps carriers avoid automation bias and weak review loops.

5 Reliable Engineering Partners For Explainable Insurance AI In The USA

1. GeekyAnts

GeekyAnts is an AI-powered digital product engineering and consulting company. Insurance teams can evaluate it for AI-enabled claims workflows, underwriting platforms, mobile insurance products, model-integrated applications, and cloud-ready engineering.

Clutch lists GeekyAnts at 4.8 with 115 reviews. Address: GeekyAnts Inc, 315 Montgomery Street, 9th and 10th floors, San Francisco, CA, 94104, USA. Phone: +1 845 534 6825. Email: info@geekyants.com. Website: www.geekyants.com/en-us.

2. Vention

Vention supports custom software, AI development, staff augmentation, and platform engineering for companies that need delivery capacity across complex systems. Its relevance to insurance AI stems from engineering support for model deployment, integrations, data workflows, and product modernization.

Clutch lists Vention at 4.9 with 101 reviews. Address: 575 Lexington Avenue, 14th Floor, New York, NY, 10022, USA. Phone: +1 718 374 5043.

3. Simform

Simform works across product engineering, AI, data, cloud, and platform modernization. Insurance organizations can evaluate it for data engineering, ML operations, app modernization, and cloud infrastructure programs that support explainable decision systems.

Clutch lists Simform at 4.8 with 86 reviews. Address: 111 North Orange Avenue, Suite 800, Orlando, FL, 32801, USA. Phone: +1 321 237 2727.

4. BlueLabel

BlueLabel focuses on generative AI, product development, agentic workflows, mobile applications, and product design. Its relevance for insurers lies in customer-facing AI experiences, workflow automation, AI product strategy, and claims or service applications that require strong UX and accountable automation.

Clutch lists BlueLabel at 4.7 with 69 reviews. Address: 18 West 18th Street, New York, NY, 10011, USA. Phone: +1 206 651 4244.

5. ScienceSoft

ScienceSoft brings experience in custom software development, cybersecurity, mobile development, IT consulting, and regulated industries. Insurance teams can evaluate it for claims automation, underwriting support tools, risk analytics, portals, and security controls around AI-enabled systems.

Clutch lists ScienceSoft at 4.8 with 42 reviews. Address: 5900 S. Lake Forest Drive, Suite 300, McKinney, TX, 75070, USA. Phone: +1 214 306 6837.

Final Thoughts

US insurance leaders can build explainable AI models that pass compliance reviews only when explainability is embedded in the product architecture, not alongside it. Underwriting and claims AI need approved data, documented features, model versioning, fairness testing, human review, and decision-level audit trails.

The real advantage will not come from the most complex model. It will come from the insurance platform that gives leaders confidence during regulatory questions, customer appeals, internal audits, or board reviews. Teams that plan AI this way can move faster by reducing rework, reputational risk, and compliance friction before production.