Blog

5 Hidden Fund Charges Exposed by an Online ULIP Calculator Before You Purchase a Multi-Asset ULIP Plan

Most people who buy a ULIP plan do so after looking at two numbers.

The projected maturity value at an assumed growth rate. And the annual Premium. Everything else in the product, the charge structure sitting underneath the headline numbers, rarely gets examined closely before the decision is made.

That oversight is expensive. Not because ULIP plans are inherently bad products. But because the charge structure of a ULIP has a compounding effect on returns over 15 to 20 years, that is far more significant than most buyers realize at the time of purchase.

A ULIP calculator, used properly before buying rather than to check projected returns, exposes this charge structure in a way that the sales illustration rarely makes obvious.

Why the Charge Structure Matters More Than the Projected Return

Two ULIP plans with identical fund performance will produce different maturity amounts if their charge structures differ. The gap between them is not visible in the fund’s NAV growth. It is visible only when the effective return on total premiums paid is calculated across the full tenure.

A ULIP calculator that models the Internal Rate of Return on the investment, accounting for all charges deducted at every stage, shows what the investor actually takes home rather than what the fund produced. These two numbers are often meaningfully different, particularly in the early years of the policy, when front-loaded charges account for the largest share of each Premium.

Here are five specific charges that a ULIP calculator exposes before purchase.

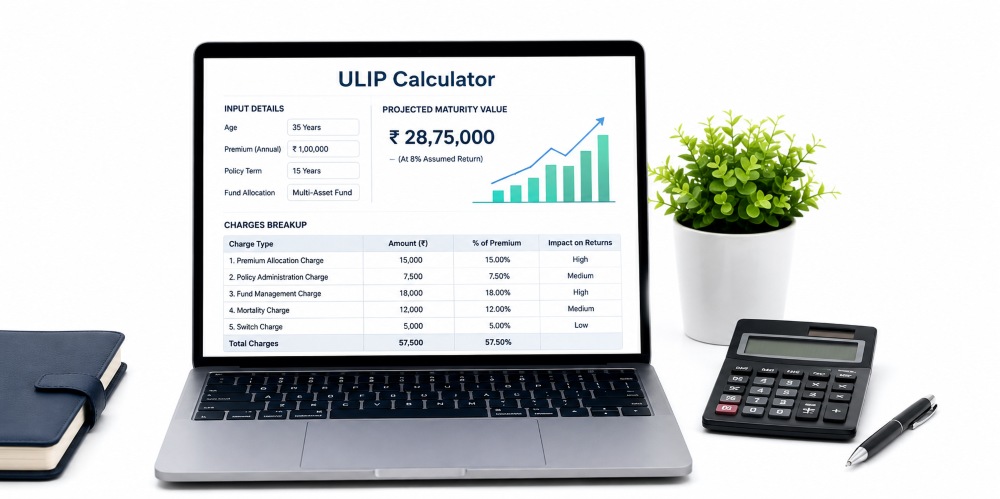

1. Premium Allocation Charge

This charge is deducted from each Premium before the remaining amount is invested in the chosen fund. It typically ranges from 2% to 5% of each Premium paid and is higher in the first few years of the policy, then declines or disappears in later years.

The effect is immediate. A Premium of 1 lakh with a 5% Premium allocation charge means only 95,000 rupees enter the fund.

A ULIP calculator shows the cumulative Premium allocation charge deducted across the full tenure. Over 15 years of annual premiums, this figure can amount to several lakhs, depending on the charge percentage and whether it reduces over time. Seeing this number in one place before buying reveals whether the plan’s charge structure justifies the investment.

2. Fund Management Charge

The fund management charge is deducted annually as a percentage of the fund value and goes toward paying the fund manager. Under IRDAI regulations, the fund management charge on unit-linked products is capped at 1.35% per annum.

This charge is invisible on a day-to-day basis because it is reflected in the fund’s NAV rather than appearing as a separate line item. The fund’s published return already reflects this charge.

What a ULIP calculator reveals is the cumulative amount deducted as fund management charge across the tenure. On a fund value that has grown to 40 lakhs by year 12, a 1.35% annual fund management charge amounts to 54,000 rupees, deducted that year alone. Compounded across the full tenure on a growing corpus, the total fund management charge is substantial.

3. Mortality Charge

The mortality charge is the cost of the life insurance component within the ULIP plan. It is deducted monthly from the fund value through unit cancellation and increases as the insured’s age increases.

A 30-year-old pays a relatively low mortality charge. The same person at 50 pays a significantly higher price. In a ULIP plan running for 20 years, the total mortality charges deducted across the tenure can be considerable, particularly if the sum at risk, the difference between the death benefit and the fund value, remains high.

A ULIP calculator models the mortality charge over the full tenure based on the insured’s age progression. This projection shows how the charge escalates in the later years and its cumulative impact on the final corpus.

4. Policy Administration Charge

This is a flat monthly or annual charge covering the administrative costs of maintaining the policy. It is typically a fixed amount, sometimes with a small annual escalation, and is deducted from the fund value through unit cancellation.

The policy administration charge can seem small, but over a 15 to 20-year tenure, the cumulative amount adds up. A ULIP calculator includes this charge in the total charge calculation, alongside the others, to show the combined drag on the fund.

5. Surrender Charge

The surrender charge applies if the policy is discontinued before the end of the five-year ULIP lock-in period under current IRDAI regulations. The fund value at discontinuation is placed in a discontinued policy fund, which earns a minimum of 4% annually and is paid out after the five-year period ends.

The surrender charge is tiered. It is highest in year one and reduces to zero after year five. On a ULIP plan surrendered in year three, the charge can represent a meaningful percentage of the accumulated fund value at that point.

A ULIP calculator that models the surrender scenario shows exactly what the investor would receive at each point during the lock-in period, compared with continuing to the planned maturity. This comparison is useful for anyone uncertain about maintaining Premium payments throughout the tenure.

Using the ULIP Calculator Before Purchase

The practical exercise is running the ULIP calculator with the actual Premium amount, the insured’s current age, the planned tenure and the fund allocation being considered. The output should show not just the projected maturity value but also the itemized charges deducted over the tenure.

Comparing this output across two or three different ULIP plan options with different charge structures reveals which plan retains more of the investment return for the policyholder rather than absorbing it in charges. The difference between a high-charge and a low-charge ULIP plan, with the same Premium over 15 years, is often significantly larger than the Premium difference between them.

Final Notes

A multi-asset ULIP plan should not be judged only by its projected maturity value. The better question is how much of the Premium actually stays invested after charges, and how much value remains if the policyholder needs to stop, switch, or surrender the plan earlier than expected.

An online ULIP calculator gives buyers a clearer view of that reality before they commit. It helps compare plans by net returns, charge impact, flexibility, and long-term suitability, rather than relying solely on optimistic illustrations. Before purchasing, investors should test different Premium amounts, policy terms, fund options, and surrender scenarios. This makes the decision more practical and less dependent on headline projections.

The right ULIP plan is not always the one showing the highest estimated maturity value. It is the one where the insurance coverage, investment structure, charges, and holding period align with the buyer’s financial goals.

Disclaimer

This article is for general informational purposes only and should not be treated as financial, investment, tax, or insurance advice. ULIP charges, benefits, returns, lock-in rules, surrender values, and tax treatment may vary depending on the insurer, policy terms, fund option, Premium amount, age, and applicable regulations.

Before purchasing any ULIP plan, investors should carefully read the official policy brochure, benefit illustration, terms and conditions, and charge schedule. It is also advisable to consult a licensed financial advisor or insurance professional to understand whether the plan is suitable for personal financial goals, risk appetite, and long-term commitments.